download our full buyer's guide

A step-by-step guide to buying a new home.

A step-by-step guide to buying a new home.

Thank you for trusting me to guide you through the home-buying process. My goal is to make the journey as smooth, informed, and enjoyable as possible. This guide is here to serve as your step-by-step reference, so you’ll always know what’s ahead and how each stage works.

Throughout the process, I’ll stay in close contact and adapt to your needs and preferences, making sure you feel confident, supported, and well-prepared from start to finish. My hope is that by the end, you’ll not only have a new home you love, but also a buying experience that felt clear, stress-free, and even a little exciting.

Buying a home is one of the biggest decisions you’ll ever make—and it helps to have someone fully on your side from the first home tour to the day you get your keys. A buyer’s agent is your advocate. Their role is to protect your interests, negotiate on your behalf, and guide you through each step with your goals front and center.

Keep in mind, the seller already has an agent whose job is to get them the highest possible price. That’s why having your own dedicated buyer’s agent isn’t just a good idea—it’s an important part of making sure your purchase is fair, informed, and as smooth as possible.

Before you start house hunting, it’s important to get a clear picture of your financial situation. This will help you set a comfortable budget, avoid surprises, and move quickly when you find the right home.

A common guideline is that your home’s price should be no more than three to five times your annual household income. Lenders, however, will look more closely at your debt-to-income ratio (DTI)—ideally keeping your housing costs at or below 28% of your income, and total debts at or below 36%.

Once you’ve reviewed your finances, the next step is to explore your mortgage options. Comparing lenders will help you find the best rates, terms, and service for your needs.

Start by gathering quotes from several reputable lenders, including both local providers and national institutions. Look beyond the interest rate—consider fees, loan programs, and the lender’s reputation for customer service.

Ask about any special programs you might qualify for, such as:

When you’re ready, apply for mortgage pre-approval. This goes beyond pre-qualification—your lender will review and verify your income, assets, debts, and credit history. You’ll receive a pre-approval letter showing the loan amount you qualify for, which strengthens your position when making an offer.

Having your pre-approval in hand signals to sellers that you’re a serious buyer and gives you a clear budget to work with as you search for your new home.

With your pre-approval letter in hand, it’s time for the exciting part—finding your new home.

Start by deciding which features matter most to you. Think about the number of bedrooms and bathrooms you need, the size and layout of the kitchen, storage space, outdoor areas, and any special features that would make daily life more enjoyable.

Once you’ve outlined your must-haves, think about the kind of neighborhood you want to live in. Factor in the quality of local schools, your commute time, proximity to shopping, dining, parks, and recreation, as well as overall safety and the general upkeep of the area. It’s also worth considering the potential for property values to increase over time so your home remains a smart investment.

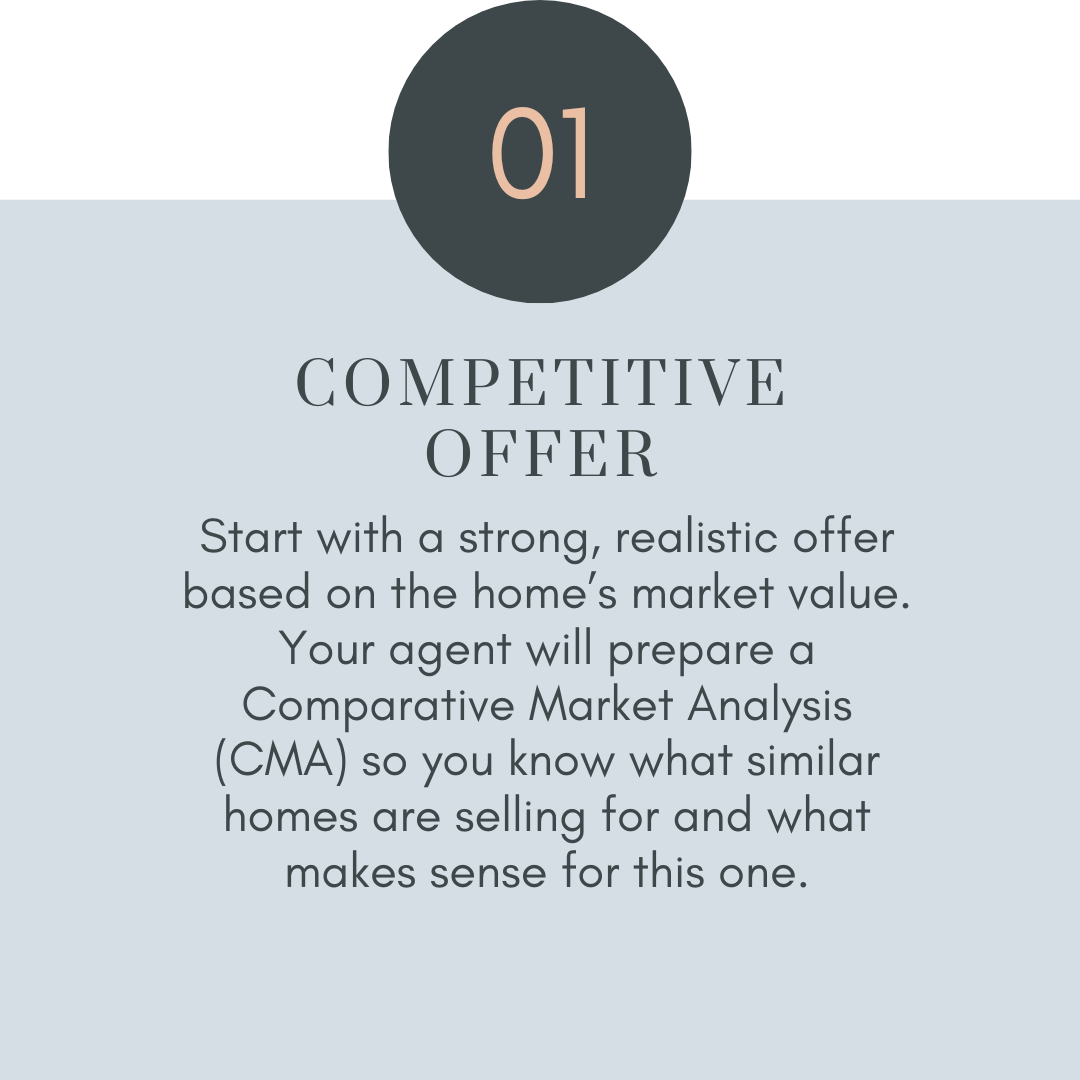

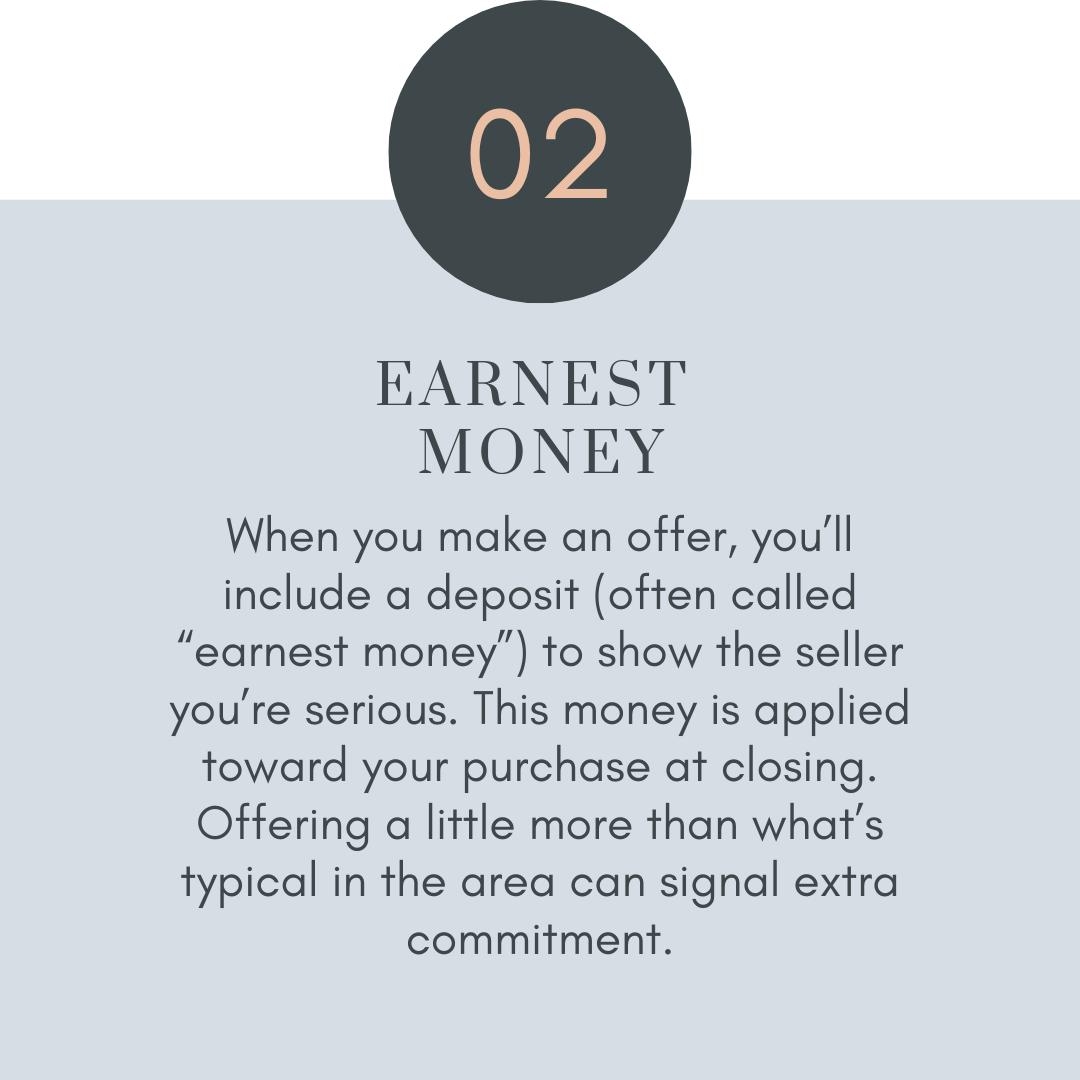

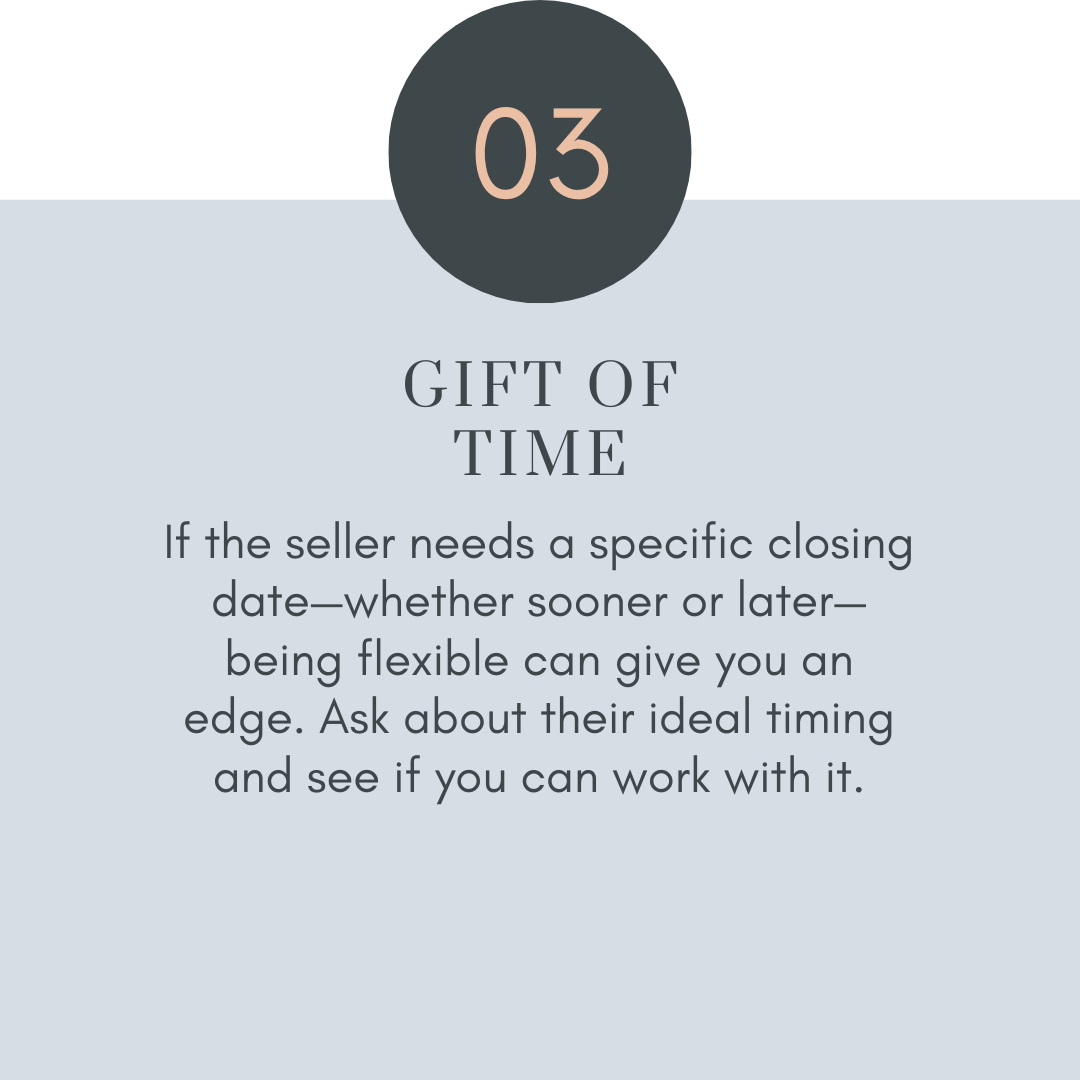

In a competitive market, the right strategy can make your offer stand out. The goal is to give the seller strong reasons to choose your offer—while still protecting your needs and budget.

Once you’ve found the right home, it’s time to make an offer. Here’s how the process typically works:

Your agent will prepare and present your offer to the seller. This will include the proposed purchase price, any contingencies (such as inspections or financing), and your preferred closing date.

If you receive a counteroffer, you can either accept it, send your own counteroffer, or decide to walk away. This back-and-forth can happen multiple times until both sides reach an agreement.

Once all terms are agreed upon and signed by both parties, you are officially under contract. — CONGRATULATIONS!

A home inspection is a professional checkup on the property, from roof to foundation, to help you understand its condition before moving forward. A licensed inspector will review the major systems, structure, and safety features, then provide a detailed report with photos and notes. If possible, attend the inspection to see issues firsthand and ask questions.

Once you have the report, you can request repairs, ask for a credit, renegotiate the price, move forward as-is, or cancel the purchase if your contract allows. For major concerns, get contractor estimates to guide your decision and negotiations.

If the home inspection finds issues, you have several options:

Ask the seller to make repairs before closing so the work is completed when you move in.

Request a credit toward your closing costs so you can handle the repairs yourself after the purchase.

Negotiate a lower sales price to offset the cost of the repairs.

Use your inspection contingency to cancel the purchase if the issues are more than you want to take on.

Accept the home as-is and move forward with the deal.

Before negotiating, it’s a good idea to get an estimate from a local contractor or repair professional so you know the real cost. Your real estate agent will guide you through this process, handle the negotiations, and use the inspection report to support your requests with the seller.

Once your offer is accepted and you are under contract, your lender will order an appraisal. An appraisal is a professional opinion of the home’s market value, based on factors such as location, condition, and comparable recent sales.

The appraisal is important because your lender will only approve a loan for the appraised value or the purchase price—whichever is lower. If the appraisal comes in lower than your offer, you may need to renegotiate the price with the seller, pay the difference in cash, or cancel the contract if you have an appraisal contingency.

Your agent will guide you through the process, explain the results, and help you decide on the best next steps if the appraised value is less than expected.

Once your offer is accepted, it’s time to start planning your move. Here’s a simple timeline to help keep everything on track.

Give 30 days’ notice if you are renting.

Schedule movers or reserve a moving truck.

Gather packing materials and start packing non-essentials.

Arrange for the appraisal and complete the title search (your lender and title company will help).

Secure a home warranty and get quotes for homeowner’s insurance.

Contact utility companies to set up service at your new home and end service at your current one.

Begin notifying important contacts of your change of address.

Continue packing, focusing on items you won’t need before the move.

Minimize grocery shopping so you have less to move.

Create an inventory of valuable items and gather any important documents.

Obtain certified checks for closing.

Schedule and attend your final walk-through.

Pack essentials for the first few nights in your new home.

Clean your current home and confirm details with your movers, including directions and your contact number.

Closing is the final step before you officially own your new home. This is when you’ll sign all the required paperwork, transfer funds, and receive your keys. Most closings take about one to two hours.

Within 24 hours of closing, you’ll do a last check of the property to ensure it’s in the agreed-upon condition and any repairs have been completed.

During your walk-through, be sure to:

Closing is typically attended by you, your real estate agent, the seller, the seller’s agent, and sometimes your lender or escrow officer. You’ll review and sign all loan, title, and transfer documents, and your payment for closing costs will be collected.

Once everything is signed and recorded, you’ll get the keys to your new home—congratulations! Take a moment to celebrate, then start settling in at your own pace.

from here to home

Home buying is a series of clear steps, and you now have a roadmap for what comes next. Use this guide as a reference as you explore neighborhoods, tour homes, review disclosures, and make decisions. If questions come up at any point—whether simple or complex—please reach out. Clear information and steady communication make the process smoother and more confident.

When you are ready, schedule a brief conversation to review your timeline, budget, and search criteria. Together, we can outline next steps, confirm your priorities, and make a plan that fits your goals.

Jacqueline works with sincere honesty, integrity, and transparency to help you meet your real estate goals: selling your home for the highest possible price in the fewest days on the market!